BENEFITS OF A SUPER LONG ENGAGEMENT

Posted on November 8, 2018

Superannuation is a long-term financial relationship. It begins with our first job, grows during our working life and hopefully supports us through our old age.

Throughout your super journey you will experience the ups and downs of bull and bear markets so it’s important to keep your eye on the long term.

The earlier you get to know your super and nurture it with additional contributions along the way, the more secure your later years will be.

Like all relationships, the more effort you put into understanding what makes super tick, the more you will get out of it.

Your employer is required to make Superannuation Guarantee (SG) contributions into your account of at least 9.5 per cent of your before-tax income. If you are self-employed you are responsible for making your own voluntary contributions, but these are tax-deductible.

CHECK YOUR ACCOUNT

The first step is to check how much money you have in super and whether you have accounts you’ve forgotten about.

You can search for lost super and consolidate all your money into one fund if you have multiple accounts by registering with the ATO’s online services.i Having a single fund will avoid paying multiple sets of fees and insurance premiums.

The next step is to check what return you are earning on your money, how it is invested and how much you are paying in fees.

If you don’t nominate a super fund or investment option, your SG money is invested in the ‘Balanced’ or default option nominated by your employer. Balanced options typically have 60-75 per cent of their money invested in growth assets such as shares, with the remainder in bonds and cash.

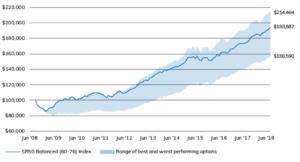

Over the past 10 years, $100,000 invested in the median balanced option would have nearly doubled to $193,887, but there was a wide range of performance (see the graph below). The best performing balanced option returned $214,464 over the same period while the worst returned $156,590.ii

The difference between the best and worst performing funds could fund several overseas trips when you retire, so it’s worth checking how your fund’s returns and fees compare with others. You can switch funds if you are not happy, but it’s never wise to do so based on one year’s disappointing return. Super is a long-term investment so get in the habit of looking at your fund’s performance over five years or more and comparing its returns with similar products.

A decade of super returns

Source: Super Ratings

STATE YOUR PREFERENCES

Default options are designed for the average member, but you are not necessarily average. Younger people can generally afford to take a little more risk than people who are close to retirement because they have time to recover from market downturns. So think about your tolerance for risk, taking into account your age, and see what investment options your super fund offers.

As you grow in confidence and have more money to invest you may want the control and flexibility that come with running your own self-managed super fund.

Also check whether you have insurance in your super. A recent report by the Australian Securities and Investments Commission (ASIC) found that almost one quarter of fund members don’t know they have insurance cover, potentially missing out on payouts they are entitled to.iii

Insurances may include Total and Permanent Disability (TPD) and Income Protection which you can access if you are unable to work due to illness or injury, and Death cover which goes to your beneficiaries if you die.

BUILDING YOUR NEST EGG

Once you understand how super works you can take your relationship to the next level by adding more of your own money. Small amounts added now can make a big difference when you retire.

You can build your super in several ways:

- Pre-tax contributions of up to $25,000 a year (including SG amounts), either from a salary sacrifice arrangement with your employer or as a personal taxdeductible contribution. This is likely to be of benefit if your marginal tax rate is higher than the super tax rate of 15 per cent.

- After-tax contributions from your takehome pay. If you are a low-income earner the government may match 50c in every dollar you add to super up to a maximum of $500 a year.

- If you are 65 and considering downsizing your home, you may be able to contribute up to $300,000 of the proceeds into your super.

You could also share the love by adding to your partner’s super. This is a good way to reduce the long-term financial impact of one partner taking time out of the workforce to care for children. You can split up to 85 per cent of your pre-tax contributions with your partner. Or you can make an after-tax contribution and, if your partner earns less than $40,000, you may be eligible for a tax offset on the first $3,000 you put in their super.

Before you make additional contributions, adjust your insurance, or alter your investment strategy, it’s important to assess your overall financial situation, objectives and needs. Better still, make an appointment to discuss how you can build a positive long-term relationship with your super.

i https://www.ato.gov.au/individuals/super/keepingtrack-%20of-your-super/#Checkyoursuper

ii https://www.superratings.com.au/2018/09/20/%20dont-panic-what-superannuation-is-teaching-thepost-%20gfc-world/

iii https://download.asic.gov.au/media/4861682/%20rep591-published-7-september-2018.pdf

RECENT POSTS

Last month FFA was honoured to WIN the 2018 “Small Business of the Year Award” at the Greater Dandenong Chamber of Commerce Business awards!

Investing successfully and improving your investment portfolio can be as much about minimising mistakes as trying to pick the ‘next big thing’. It’s all about taking a calm and considered approach and not blindly following trends or hot tips.

Winter 2024

With Winter now officially underway, some might be heading north to warm up and others may lean into the cold on the snowfields. Whichever you choose, don’t forget the approaching end of financial year.

Company Addresses

Business Address

49 Robinson St

Dandenong VIC 3175

Postal Address

PO Box 856

Dandenong VIC 3175

e hello@financialfoundations.com.au

p (03) 9793 3722

Quick Links

Stay Connected

Copyright © 2025 Financial Foundations. All rights reserved | Website by Socialisd.